Yana credit account is a sustainable financing option for your business. We designed it so that you never run out of funds on rainy days or to step into your next level of growth!

Here is all you need to know about using it.

Yana Credit Account Is Not Like Your Typical Loan

First things first, Yana’s credit is not an emergency loan or termed loan. It is a credit line specifically tailored for ambitious businesses. You can’t use it to finance personal expenses and it is made to cater to business payments for bills, services, equiments and inventory.

Benefits Of A Credit Account On Yana.

There are a lot of benefits to choose a Yana credit account.

- You don’t need any physical collateral or cash debenture that is above 100% of your approved credit line like a traditional financier would request.

- Transparent pricing and fees.

- Flexible tenure structure.

- One time application process.

- Revolving credit. As you pay each due payment, money becomes available to spend again.

- Line of credit. Get approved for a limit, spend what you need per time.

- Halal financing option.

How To Apply For A Credit Account.

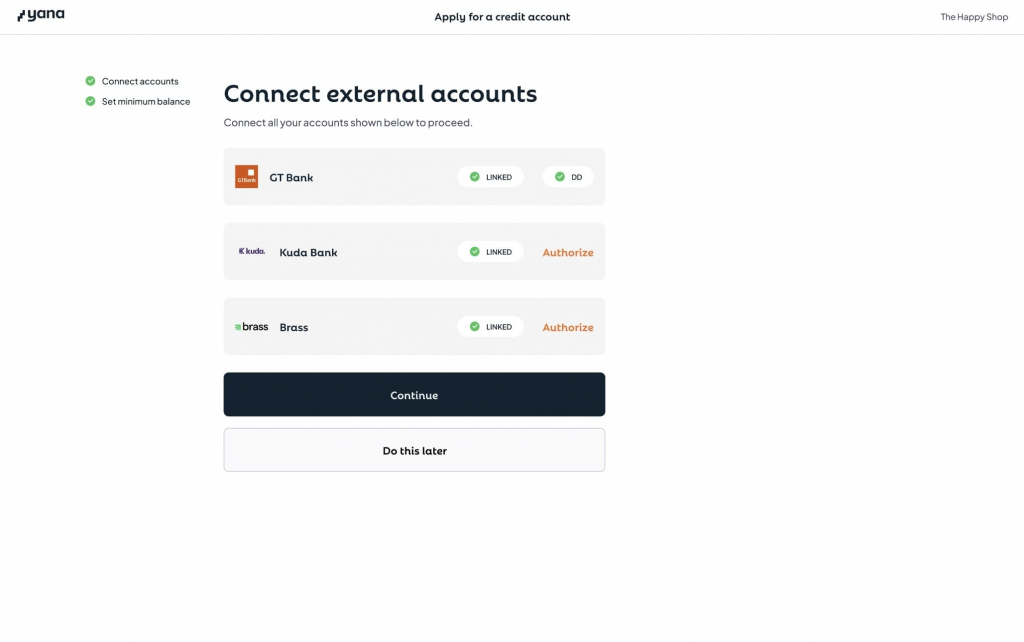

Creating your credit account is as easy as ABC. Once your deposit account is open and you have your existing banks and other financial institutions connected and authorized, you would tap on the ‘apply for credit‘ button.

If you don’t have all your banks connected, you’d be prompted to do so.

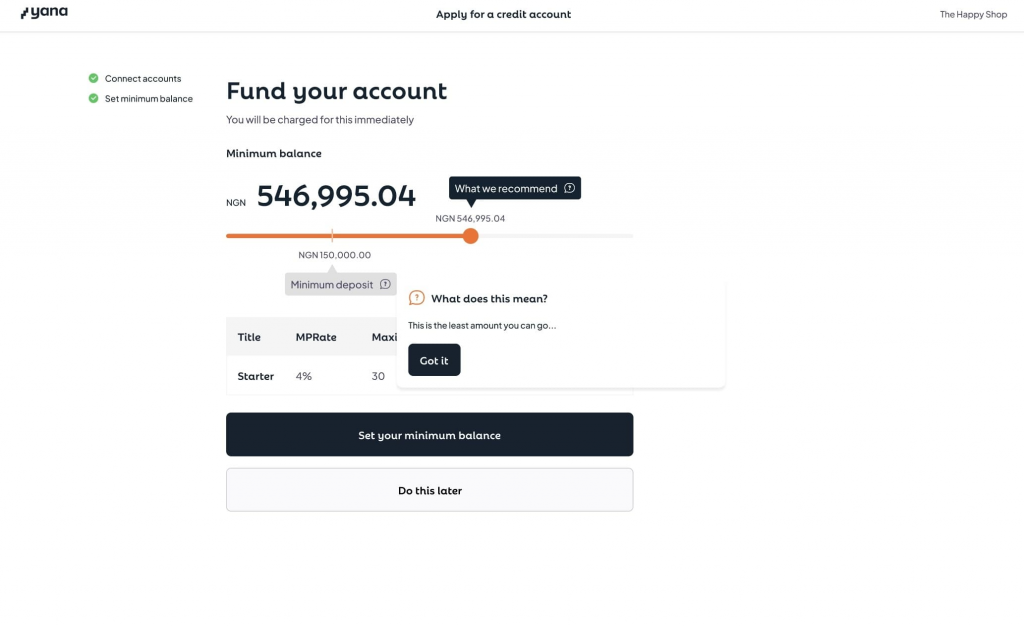

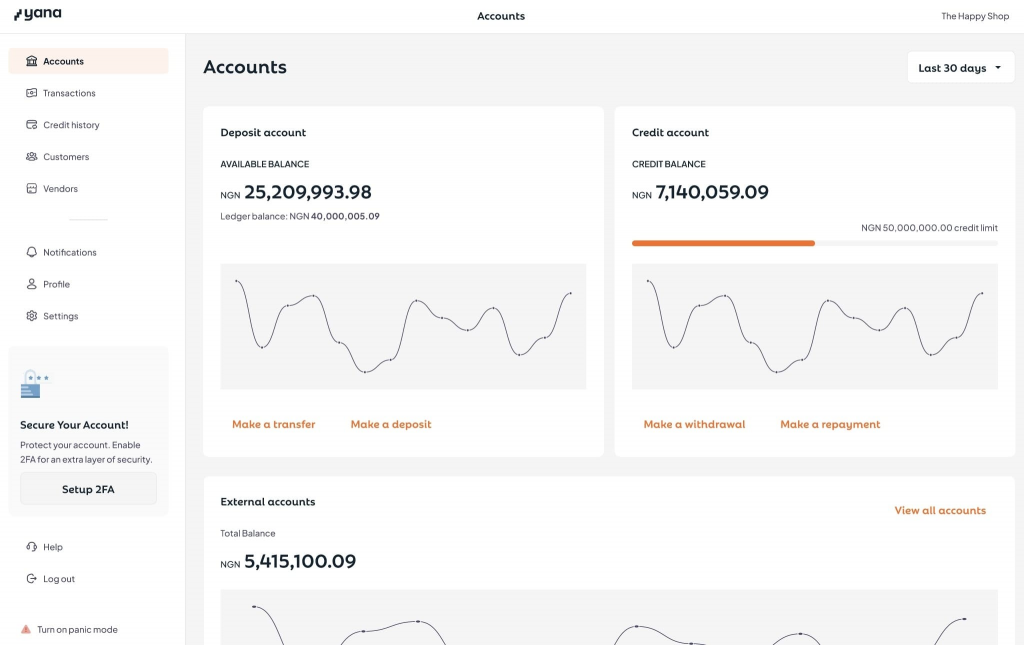

When or if all your banks are connected, you’d get a credit limit. To secure this limit, there’s a 15% cash collateral. The deposit on your minimum balance does this job. Remember that your minimum balance earns a yield at 24% per annum paid into your deposit account on the 2nd of every month and it is fully withdrawable as long as you don’t have any outstanding repayment. You can read more about minimum balances here.

You can deposit less than the recommended amount into your minimum balance. However, it would reduce your credit limit. You can also not have a minimum balance less than 150,000 Nigerian Naira as our lowest credit limit is 1 million Nigerian Naira. Once you complete your deposit, your credit account is opened and active. Voila! Time to do transactions.

How Transactions Work With The Credit Account

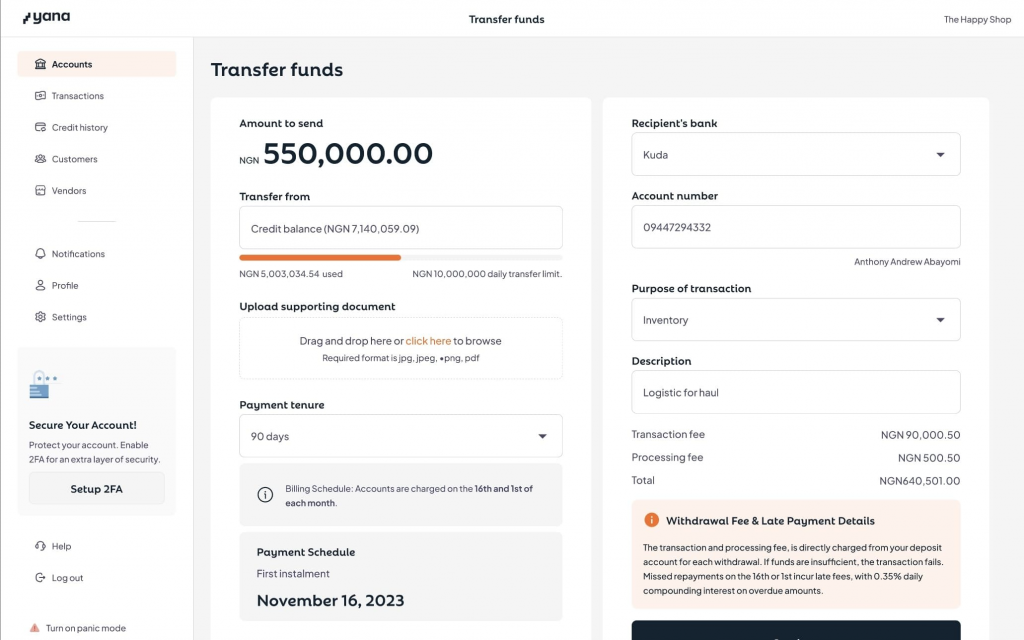

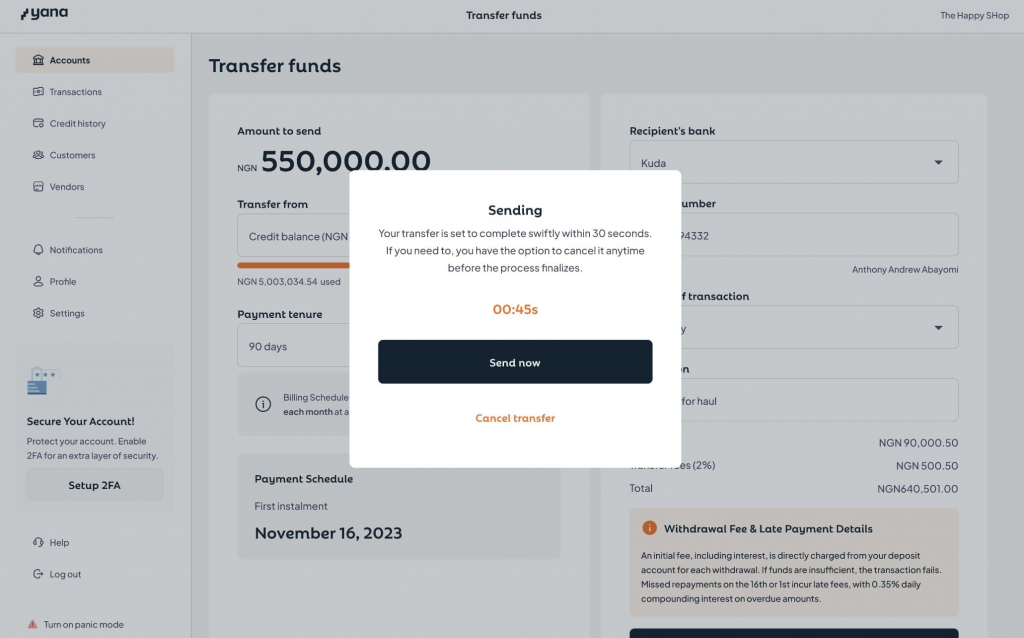

Sending money from your credit account is as simple as sending money from a regular deposit account. You select the beneficiary, choose the tenure that’s most convenient for you, choose a purpose for the transaction, upload supporting documents and confirm the transaction with an otp number that will be sent to you.

The processing and transaction fees are charged upfront from your deposit account. Ensure you have sufficient money for the transaction to ensure it goes through successfully. Your transaction will immediately go into pending once you confirm, allowing you time to cancel the transaction if the need be.

It will be authorized 15 minutes afterwards and the vendor, supplier or contractor will receive the money anywhere from a few minutes to 24 hours. This totally depends on congestion and network with our payment processors and NIBBS.

You will receive a mail after every successful transaction and you can find the repayment schedule on your email.

Understanding Pricing And Repayment

Here’s some few unique things to understand:

- Processing fees: charges that are incurred to process the transaction including insurance, third party processors etc. It is a standard 1.5%

- Transaction fees: this is the cost of the transaction. More or less, the interest. It is dynamic and dependent on prevailing rate on your credit account at the time of the transaction and tenure chosen. Our rates are currently 3% to 5% and the maximum tenure is 180 days.

- Principal repayment: because all fees are paid upfront, you only pay back the principal amount. We charge on the 1st and 16th of every month only, except overdue payments. We charge the principal repayment accrued on those dates from the last charge. We primarily charge your deposit account on Yana and will charge your other banks otherwise. Charging your other banks might incure extra charges, and these charges are dependent on the method and partner involved in collections.

- Late fees: late fees are charged at 0.35% daily COMPOUNDING interest. This fee kicks in on the 3rd and 18th of every month. It is always better to pay a part, than not pay at all.

- Estimated repayment schedule: when you choose the halal option while making a transaction, we do not term your payment to a period. This means that we will only be able to provide you with estimated amounts that we will charge on the payment dates and the period of time it will take, not more than 180 days. If your payment extends past 180 days, additional dates will be automatically added to your payment schedule. Halal repayments are 20% of your sales during the period under consideration till principal is paid back.

- Rebates: if you finish your payment before the final due date, we would refund part of the transaction fee, an equivalent of 60% of the not yet due period to your deposit accounts.

Revolving Line Of Credit.

Being a line of credit means that you can manage how you spend from your credit account.

If you have a limit of 5,000,000 Nigerian Naira for instance, you can spend 500,000 Nigerian Naira on a new equipment for your store today, 2,000,000 Nigerian Naira on some inventory next week and 800,000 Nigerian Naira to pay a contractor the day after. This means you don’t have to incure fees on money you are not ready to spend and have repayment schedules for money you haven’t invested yet.

Remember that your credit line is revolving. This means that anytime you make a principal payment, it becomes available on your credit balance from the 3rd and 18th to spend again. If you have any more questions, do not hesitate to contact our support team on swift@yana.finance and we’d be happy to provide more clarity.